They say it’s all about timing, and it’s particularly true when it comes to paying for loans. The most significant factor weıghıng in your credit score is paying back your credit card and loan balances on time.

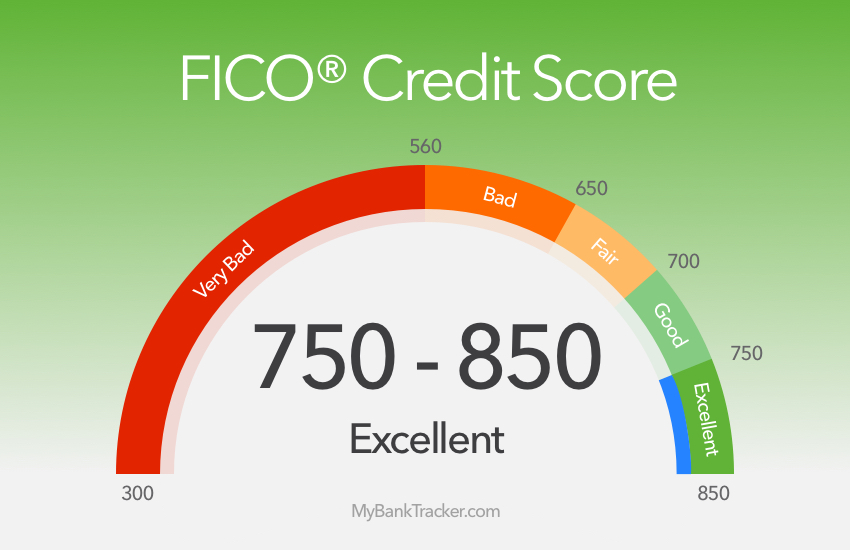

Your credit score is used by lenders and creditors to decide whether to offer you products including mortgages, credit cards, and auto loans. Your credit payment history is the single largest aspect that affects your credit score.

Your payment history is a record of your payment actions on all credit accounts, such as loans and credit cards. Read on to discover how your credit score is affected by your payment history.

How Does Payment History Affect Credit Scores?

Payment history provides an overview of how you paid your bills to lenders. Your payment history will share if you regularly paid on time, skipped some payments, or had outstanding debt sent to collections.

If you miss payments or don’t make payments at all, your credit score decreases and you are perceived by lenders to be a greater risk when it comes to lending you money.

Your credit score provides lenders with an indication of how likely your loans are to be paid back. A payment history that depicts payments being made on time over a certain duration will raise your credit score.

At What Point Is a Late Payment Reported?

If you are at least 30 days past due, late payments will go on your credit reports and impact your score. Before this happens, you may have to pay a late fee to your lender or card issuer, but a late payment cannot be reported to the credit bureaus legally.

A late payment will appear on your payment history if you exceed the 30-day mark. The longer you delay payment, the more it negatively affects your credit score. Timely payments are essential to maintaining a healthy credit history.

Getting Smarter About Your Credit and Debt

If you are unable to pay your outstanding bills, your payment history on your credit reports will be impacted for a long time.

Late bill payments will remain for up to seven years on your credit report, and accounts submitted to collections can stay for seven years as well.

It is important to develop good credit habits so that you can improve and strengthen your credit history and credit score. To better your payment habits, here are some things you can do.

Pay Your Bills On Time

Your payment history accounts for roughly 35% of your FICO credit score, so an effective way to boost your credit score is to make payments on time.

Through automatic payments, you can benefit from getting your credit card bill paid automatically on or before the due date. Or, use your online banking’s bill payment feature to pay your bills online easily.

Whenever feasible, try paying more than what’s due. This helps to pay off debt more quickly, save on interest rates, and can strengthen your credit score.

Make Your Accounts Current

Older negative data can have less effect on your credit score than more recent negative records. So, the longer you pay the bills on time, the better your payment history, and subsequently your credit score, will be.

Paying the minimum on credit accounts can help make sure your account is current and in good standing.

Practice Making Payments

Find out how much the average monthly payments will be for a new loan from a lender, then transfer this balance for three to four months into a separate savings account. If you are able to bear this cost easily, you can afford these payments.

Also, you’ll have money in your savings by the end of the practice phase that you can use to make a down payment, reduce the sum you borrow, or place into an emergency fund.

Conclusion

Your payment history is the track record of your credit accounts being paid. It is the most powerful credit factor because without a strong payment history you cannot have a good credit score.

In many cases, it is someone’s credit card payment history that ends up ruining their credit score. To make sure that doesn’t happen to you, don’t buy things you don’t need if you don’t have the cash for it.