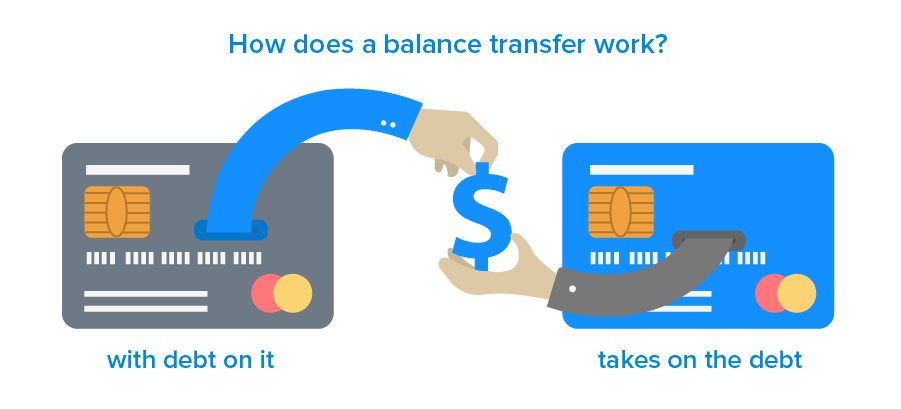

Balance transfer cards with 0% introductory APRs offer a strategic way to manage and eliminate existing credit card debt. By shifting balances to these types of cards, you buy time to pay off the debt without accruing interest. This guide presents top options from 2020, tailored to help you save on interest while handling repayment efficiently.

Citi Simplicity® Card

The Citi Simplicity Card features a 0% APR on balance transfers and no annual fee.

While it charges a transfer fee of either $5 or 5% (whichever is higher), it stands out by charging no late payment fee.

Key Advantages of Citi Simplicity

This card is ideal if you prefer predictability—you’ll never face a penalty interest increase due to late payments as long as you’re up to date.

It’s also accessible to users who want a straightforward, fee-light balance transfer strategy without surprising costs.

Discover It® Balance Transfer

The Discover It Balance Transfer card grants an 18-month 0% APR for balance transfers.

Besides helping reduce interest, it offers a 5% cashback on rotating quarterly categories and 1% on all other purchases.

Rewards Plus Debt Relief

If you’re looking to reduce interest and also earn cash back while paying off debt, this card combines both benefits.

And it imposes no annual or foreign transaction fees, adding to its appeal for frequent and cost-conscious users.

Wells Fargo Platinum Card

With 0% APR for 18 months on qualifying purchases and balance transfers, the Wells Fargo Platinum card is another solid choice.

It requires a 3% transfer fee for transfers made within the first 120 days and does not charge an annual fee.

When Wells Fargo Makes Sense

This card suits those seeking an extended interest-free window and already qualifying credit.

With the 3% fee structure, it’s important to calculate break-even points based on debt size and repayment timeline.

Citi® Diamond Preferred® Card

The Citi Diamond Preferred card provides 21 months of 0% APR on balance transfers and 12 months on purchases.

It charges a 5% transfer fee (minimum $5) and later resumes interest at 15% to 25%. It also includes access to Citi Entertainment.

Clear Benefits and Considerations

The long promotional period offers substantial breathing room for repayment.

If you’re comfortable managing timing and payments effectively, the extended 0% promotion can be a powerful tool.

Chase Freedom Unlimited®

Chase Freedom Unlimited has no annual fee and includes a sign-up bonus.

It also provides 0% introductory APR on both purchases and balance transfers for 15 months, along with flexible redemption options.

Smart Redemption Flexibility

This card is great for users who want simplicity plus low-cost debt transfer.

You can redeem rewards as statement credits, cashback, gift cards, experiences, or travel—offering useful flexibility.

Conclusion

Balance transfer cards in 2020 like those from Citi, Discover, Wells Fargo, and Chase provided valuable solutions for debt relief. Each card features unique perks—whether long 0% APR terms, rewards earning, or fee-free options. Selecting the best one depends on your repayment plan, spending style, and payoff timeline. Using one wisely can save money, reduce stress, and pave the way toward financial health.